Business Funding Guides

Expert advice on getting approved for business funding

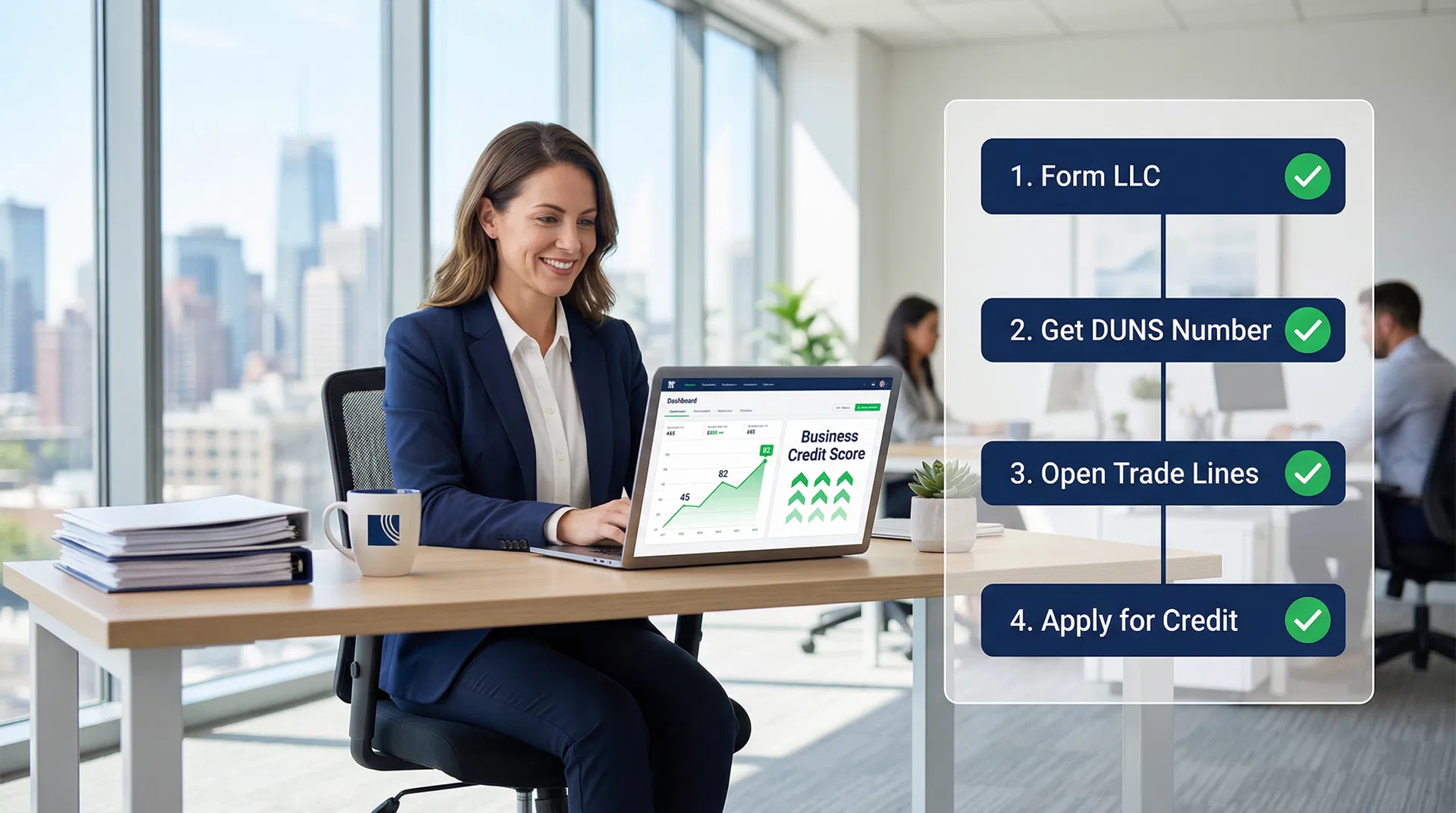

How to Build Business Credit from Scratch: A Step-by-Step Guide (2026)

Building business credit requires 8 deliberate steps: form a legal entity (LLC/corporation), get an EIN, open a business bank account, register for a DUNS number, establish 3–5 vendor trade lines, open a business credit card, apply for a business line of credit, and monitor your reports. Done correctly, you can reach a PAYDEX score of 80+ within 12 months — unlocking lower rates, larger loan amounts, and financing without a personal guarantee.

Business Line of Credit vs. Business Credit Card: Which Is Right for Your Business? (2026 Guide)

A business line of credit ($10K–$500K at 8–35% APR, no grace period) and a business credit card ($1K–$100K at 15–29% APR, 21–55 day grace period) serve different purposes. Use a credit card for everyday spending you can pay monthly — it's free financing plus rewards. Use a line of credit for large cash needs over $50K or balances you carry 30+ days. Most established businesses benefit from both.

Seasonal Retail Financing: How to Fund Holiday Inventory, Black Friday Prep & Cash Flow Gaps (2026 Guide)

Seasonal retail financing lets you fund holiday inventory, Black Friday prep, and cash flow gaps with lines of credit ($10K–$250K at 10–25% APR), inventory financing ($10K–$2M at 8–18% APR), and merchant cash advances. Apply in August — not October — to secure the best rates before peak season.

Retail Equipment Financing: Fund Your POS Systems, Fixtures & Store Technology (2026 Guide)

Retail equipment financing lets you acquire POS systems, display fixtures, refrigeration units, security systems, and store technology for $5,000–$500,000 at 8–20% APR with monthly payments instead of large upfront costs. Most retailers qualify with 12+ months in business and 600+ credit score.

How to Finance a Retail Store Expansion: 6 Funding Options for Growth (2026)

Complete guide to financing retail expansion covering 6 funding options from $50K-$5M. Compare SBA loans (6-13% APR), equipment financing, lines of credit, and commercial real estate for opening new locations, renovations, and multi-store growth. Get approval in 3-10 days with 620+ credit score.

Inventory Financing for Retail: Get $10K-$2M for Seasonal Stock (2026 Guide)

Complete guide to inventory financing for retail businesses. Access $10K-$2M at 8-18% APR with 3-10 day approval for seasonal inventory, bulk purchasing, and new product lines. Compare inventory loans, lines of credit, and purchase order financing. Credit scores 600+ qualify.

Retail Store Financing: Get $5K-$2M for Inventory, Expansion & Equipment (2026 Guide)

Complete guide to retail business financing covering 7 funding options from $5K-$2M with 24-72 hour approval. Compare inventory financing, equipment loans, working capital, and SBA programs for retail stores. No collateral options available for credit scores 580+.

Medical Practice Financing Guide: Complete Funding Options for Healthcare Providers 2026

Complete guide to medical practice financing covering equipment loans, practice acquisition financing, working capital, expansion funding, and specialized healthcare lending for doctors, dentists, and veterinarians.

Construction Financing Guide: Complete Funding Options for Contractors and Builders 2026

Complete guide to construction financing covering construction loans, equipment financing, lines of credit, SBA loans, invoice factoring, and bonding. Includes qualification requirements, cost analysis, and real-world contractor scenarios.

E-Commerce Financing Guide: Complete Funding Options for Online Businesses 2026

Complete guide to e-commerce financing covering inventory financing, merchant cash advances, business lines of credit, SBA loans, and revenue-based financing. Learn qualification requirements, costs, and which option fits your online business growth stage.

Restaurant Financing Guide: Complete Funding Options for 2026

Complete guide to restaurant financing covering equipment loans, working capital, SBA loans, lines of credit, and alternative funding. Learn qualification requirements, costs, and which option fits your restaurant's growth stage.

Bank Loans vs Online Lenders: Complete Comparison Guide 2026

Compare traditional bank loans (5-13% APR, $50K-$5M+, 4-12 weeks approval) vs online lenders (8-99% APR, $5K-$500K, 24-72 hours). Learn qualification requirements, costs, and when to choose each option.

Collateralized vs Non-Collateralized Business Loans: Complete Comparison Guide 2026

Compare collateralized loans (5-12% APR, $50K-$5M+, requires assets) vs non-collateralized loans (8-35% APR, $5K-$500K, no collateral). Learn qualification requirements, costs, and when to choose each option.

Fixed Rate vs Variable Rate Business Loans: Complete Comparison Guide (2026)

Compare fixed rate vs variable rate business loans. Learn which option saves money, when to choose each type, and how interest rates impact your business financing costs in this comprehensive 2026 guide.

Short-Term vs Long-Term Business Loans: Complete Comparison Guide (2026)

Compare short-term vs long-term business loans across interest rates, loan amounts, approval speed, monthly payments, and total cost. Learn which loan term matches your investment timeline, cash flow capacity, and business goals with side-by-side tables and real-world scenarios.

Secured vs Unsecured Business Loans: Which is Right for Your Business?

Understand the key differences between secured and unsecured business loans, including collateral requirements, interest rates, approval criteria, and which option best fits your business needs.

Business Term Loan vs Business Line of Credit: Which Is Right for You?

Choosing between a business term loan and a line of credit? This comprehensive guide compares costs, qualification requirements, and use cases to help you make the right financing decision for your business.

Invoice Factoring vs Invoice Financing: Complete Comparison Guide 2026

Invoice financing is a loan using your invoices as collateral—you collect payment from customers and repay the lender (45-60% APR typical). Invoice factoring means selling your invoices to a factoring company that collects payment directly from your customers (50-80% APR typical). Choose financing if you want to maintain customer relationships and have strong collection capabilities. Choose factoring if you want to outsource collections, have bad credit, or need higher capital limits.

Equipment Financing vs Equipment Leasing: Which Option Is Right for Your Business?

Equipment financing (loans) means you own the equipment immediately with higher monthly payments but lower long-term costs. Equipment leasing means you rent with lower monthly payments and easier upgrades. Compare ownership, costs, tax benefits, and qualification requirements to choose the right option for your business.

Merchant Cash Advance vs Business Term Loan: Which Is Right for Your Business? (2026 Guide)

Compare merchant cash advances and business term loans side-by-side. Learn the costs (40-200% vs 6-30% APR), approval times (24 hours vs 3-90 days), and when to choose each financing option for your business needs.

SBA Loan vs Business Line of Credit: Which Financing Option Is Right for Your Business?

Compare SBA loans and business lines of credit to determine which financing option best suits your business needs. Learn about interest rates, approval times, funding amounts, and when to choose each option.

Merchant Cash Advance: Complete Guide to MCA Funding in 2026

Comprehensive guide to merchant cash advances (MCAs): how they work, costs, pros/cons, and when to use this fast but expensive funding option for your business.

Invoice Factoring: Complete Guide to Selling Your Receivables for Cash

Learn how invoice factoring works, typical rates and fees, and whether selling your accounts receivable is the right cash flow solution for your business.

Business Line of Credit: Complete Guide to Revolving Credit for Small Businesses

Learn how business lines of credit work, compare secured vs unsecured options, understand rates and fees, and discover when revolving credit makes more sense than term loans for your business.

Startup Business Loans: Complete Guide to Funding a New Business in 2026

Starting a business requires capital, but securing funding as a startup presents unique challenges. Traditional banks reject over 80% of small business loan applications, and startups face even steeper odds. This comprehensive guide examines every startup financing option available in 2026, from SBA microloans to merchant cash advances.

How to Get a Business Loan with Bad Credit: Complete Guide

Discover how to get a business loan with bad credit. Learn about alternative lenders, secured loans, credit repair strategies, and approval tactics for credit scores below 600.

Business Credit Cards: Complete Guide to Corporate Credit Cards for Small Businesses

Comprehensive guide to business credit cards: types (cash back, travel rewards, low-interest, charge cards), qualification requirements (1+ years, $50K+ revenue, 670+ credit), costs (15-25% APR, $0-$695 annual fees), benefits (1-5% rewards, expense tracking, building business credit), and when to use them vs alternatives.

Working Capital Loans: Complete Guide to Financing Your Business Operations

Comprehensive guide to working capital loans: how they work, types (term loans, lines of credit, invoice financing, MCAs), costs (8-30% APR for traditional lenders, 40-200% for alternatives), qualification requirements, appropriate use cases, and alternatives.

Invoice Factoring: Complete Guide to Accounts Receivable Financing

Comprehensive guide to invoice factoring: how it works, costs (1-5% per 30 days = 12-60% APR), recourse vs non-recourse, qualification requirements, advantages, disadvantages, and when factoring makes sense for B2B businesses.

Merchant Cash Advance: Complete Guide to MCA Financing for Small Businesses

Comprehensive guide to merchant cash advances: how they work, costs (1.1-1.5x factor rates), qualification requirements, advantages, risks, and when MCAs make sense for your business.

Business Lines of Credit: Complete Guide to Flexible Business Financing

Comprehensive guide to business lines of credit covering secured vs unsecured options, qualification requirements, application process, costs, advantages, disadvantages, and strategic use cases. Learn how revolving credit can help manage cash flow gaps and seasonal needs.

Equipment Financing: Complete Guide to Funding Business Equipment

Comprehensive guide to equipment financing covering equipment loans, leases, lines of credit, qualification requirements, application process, costs, tax benefits, and alternatives. Learn how to finance machinery, vehicles, technology, and other business equipment.

SBA Loans: Complete Guide to Small Business Administration Financing

Comprehensive guide to SBA loans covering 7(a) loans, 504 loans, microloans, qualification requirements, application process, costs, and alternatives. Learn how to secure government-backed financing with low rates and long terms for your small business.

Small Business Loans: Complete Guide to Financing Your Business in 2026

Comprehensive guide to small business loans covering SBA loans, term loans, lines of credit, equipment financing, and more. Learn qualification requirements, application process, costs, and how to choose the right financing for your business.

Your Shortcut to Business Funding in Under a Week

Get approved for business funding in 24-48 hours and receive funds within a week. Learn about fast funding options including merchant cash advances, business lines of credit, invoice factoring, and short-term loans that skip the lengthy bank approval process.

Flexible Business Loans Made Easy

Discover six flexible business loan options with fast approval, minimal requirements, and adaptable repayment terms. Get funded in 24-48 hours even with credit challenges.

Your Shortcut to Business Funding in Under a Week

Bad Credit Business Loans: Get Approved Despite Poor Credit

Business Funding for Trucking Companies - Fast & Flexible Capital

How to Get Emergency Loans Without Endless Paperwork

Accounting Practice Financing Solutions

Real Estate Business Funding Options

Veterinary Practice Financing for Equipment and Expansion

Quick Funding for Your Construction Biz

Retail Store Financing Options Explained

Dental Practice Financing Fast and Flexible

Auto Repair Shop Financing Solutions

Childcare Center Funding for Expansion and Upgrades

Fitness Center Funding for Growth and Equipment

Law Firm Financing for Growth and Technology

Restaurant Business Funding Made Simple

Medical Practice Loans Fast and Flexible

Boost Your Barbershop with Smart Financing

Beauty Business Loans in No Time

Get Your Trucking Loan Approved Today

Restaurant Funding: Fast Capital for Food Service Businesses